For all the volatility and uncertainty in the economy and financial markets, high yield bonds have continued to attract investors over the last two months. Here are some of the metrics that are being factored into the assessment of potential relative value opportunities in this asset class.

Rebound

As of May 5, the JPMorgan High Yield Bond Index has recovered 11.68% since the high yield market bottomed on March 23, with BB (+14.12%) and B (+12.07%) outperforming CCCs (+8.02%). Meanwhile, BB, B and CCC-spreads of 547bps, 856bps, and 1484bps, respectively, compared to a low in April of 501bps, 854bps, and 1455bps.

The two best days for high yield in the past 30 years were March 26, the day after the Senate passed the CARES Act, and April 9, the day the Federal Reserve detailed programs to support liquidity in certain parts of the corporate bond market.

Distressed Bonds

The distressed universe for bonds in April decreased by half the prior months’ surge. Specifically, the amount of bonds trading sub-$70 decreased by $73bn m/m to $153bn or 11.6% of the universe. Energy, services, and retail accounted for 57%, 6%, and 5%, respectively, of bonds trading below $70.

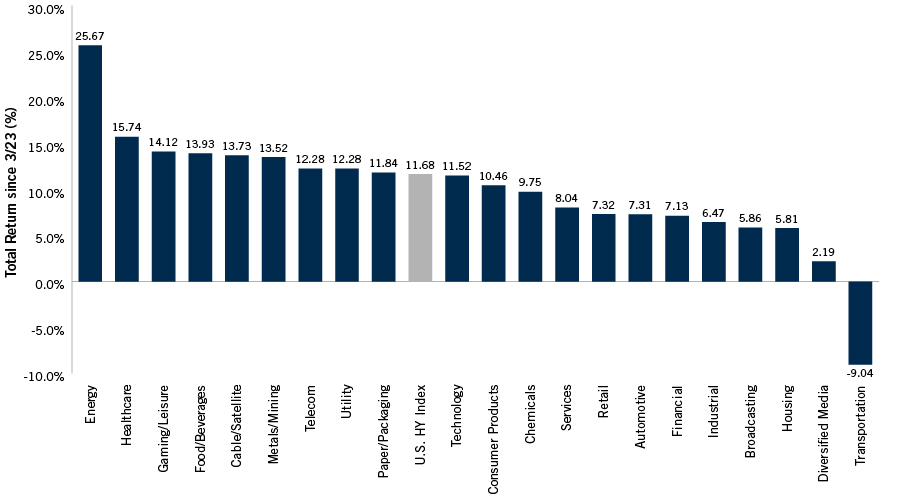

Energy Charge

Energy has led all sectors since the market bottomed on March 23. As of May 5, spreads dropped to 1493bps, down from as high as 2395bps in late March, according to JPMorgan. But while energy bonds have now recovered 25.67% off the March 23 low, they are still down -31.99% year-to-date.

HIGH-YIELD BOND SECTOR PERFORMANCE

Source: JPMorgan

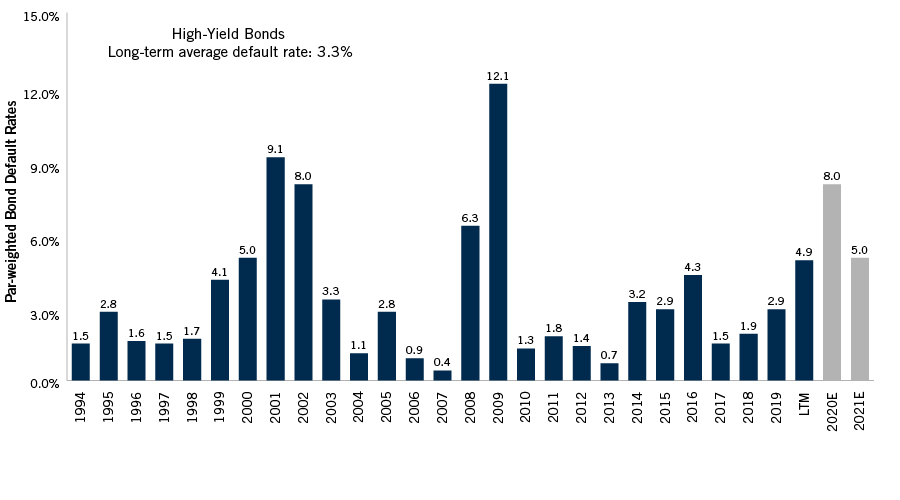

Defaults

As of April 23, the par-weighted default rate for high yield overall was 4.71%, as opposed to the long-term average default rate of 3.3%, but J.P. Morgan analysts are forecasting a default rate of 8% for 2020.

HIGH-YIELD BONDS

Long-term average default rate: 3.3%

Source: JPMorgan

Bankruptcies

A record high 19 companies filed for bankruptcy or missed an interest payment in April and one company completed a distressed exchange, according to J.P. Morgan.

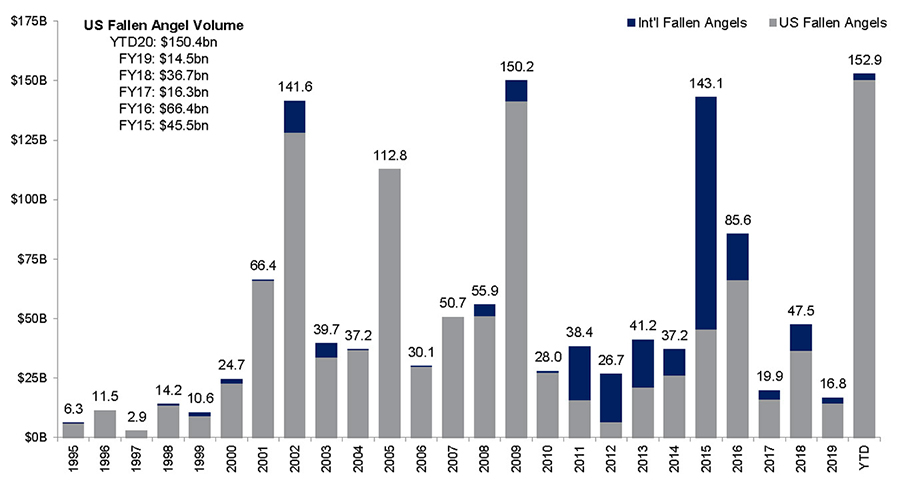

Fallen Angels

Fallen angels offer one of the more attractive potential investment opportunities in the high yield market. However, as the number of downgrades of investment grade issuers continues to grow, caution, selectivity, and risk management will be key.

FALLEN ANGELS’ GLOBAL VOLUME HAS ALREADY BROKEN RECORD

Source: JPMorgan as of April 17, 2020

The Seix Approach

Seix seeks to create value through a sound, transparent, and repeatable process that leverages our competitive advantages and aims to capture upside potential while limiting downside risk.

Critical to achieving this is in-depth fundamental, bottom-up credit analysis and a strict sell discipline.

Our high quality high yield strategy focuses primarily on BBs and Bs and liquid U.S. dollar issues (issuer size > $175 million) with multiple market makers.

Our full market high yield strategy focuses on the entire U.S. dollar high yield universe, including CCCs, and includes: opportunistic allocation to defaulted bonds (<5%); liquid U.S. dollar issues (issuer size > $175 million; $200 million if CCC); and multiple market makers.

Both strategies look for companies with: durable business models; meaningful asset coverage; solid managements with the wherewithal to pay down debt and/or invest in businesses at attractive rates of return; and ample liquidity sources such as cash, revolvers, access to securitization markets and/or non-core assets to sell.

Portfolio managers have the final say over decisions to purchase including price and allocation. They consider market price vs. expected take out –either par or recovery value, internal credit rating vs. pricing, structure review, and relative performance of security within a sector, particularly in out of favor industries.

The credit process is focused on identifying the issuers in the high yield market that offer compelling risk-adjusted return potential. A formal credit review is triggered if an issue’s price falls more than 10% relative to peers. Regarding structure risk, we focus on covenant quality, convexity of both individual securities and the portfolio, and the issue’s priority within the issuer’s capital structure.