Why institutional investors from around the world have chosen Seix for structured credit vehicles.

With $18.2 billion of fixed income assets under management as of December 31, 2019*, Seix Investment Advisors has developed a significant institutional following through multiple credit cycles. A big part of that story is how far Seix’s leveraged finance platform has come since it launched in 2006.

With collateralized loan obligations (CLO) increasingly popular among banks and insurers around the world, Seix has managed 15 CLOs (and recently closed on its ninth since the financial crisis— Mountain View CLO XV), bringing its total CLO assets under management to approximately $3.8 billion*. Like its other CLOs, this new offering focused on credits with:

–Solid asset protection;

–Improving cash flow used to grow the business and/or de-leverage the balance sheet;

–Seasoned capable management team that has gained our analysts’ confidence;

–Definable liquidity sources to fund the company’s business plan; and

–A strong competitive industry position.

* Includes AUM of two CLOs managed by an affiliate that shares staff with Seix.

That meant striving to identify the strongest and most undervalued loans with the highest return per unit of risk—and identifying the assets of leveraged loan issuers with a solid margin of safety and multiple levers to pull to generate liquidity, especially in difficult markets.

The Team

Spearheading Seix’s CLO efforts are George Goudelias, managing director, head of leveraged finance, and John Wu, managing director, head of structured credit. With 33 years of industry experience, Goudelias serves as senior portfolio manager for all leveraged loan portfolios. Wu has 23 years of experience in the financial industry. He led CLO structuring and banking at multiple sell-side firms including Deutsche Bank and UBS, and also was head of structured products at CIFC.

The View from Mountain View

Named after Seix’s former address in Upper Saddle River, NJ, Mountain View XV was positioned as a managed cash flow CLO and issued notes collateralized primarily by broadly syndicated leveraged loans. Arranged by Goldman Sachs, one of the world’s largest CLO underwriters (according to Standard & Poor’s), this CLO has a two-year non-call provision and a five-year reinvestment period with a final maturity of 13 years.

What distinguished this particular CLO was the number of challenges the Seix team had to overcome as market conditions changed.

Tapping the Japanese Institutional Market

The process started in late summer of 2019, and Japanese investors were high on the list of prospects.

Faced with negative yields in their own country, Japanese institutions have long been attracted to AAA-rated tranches in CLOs. However, by the fourth quarter of 2019, nervous regulators imposed stricter monitoring requirements.

Assuaging Concerns

The second challenge came when market liquidity dried up toward the end of 2019 as the yield curve inverted, but Seix’s demonstrated skill in portfolio construction and assessing compensation for risk helped Mountain View XV get off the ground.

With a team of seasoned portfolio managers and credit analysts backed by experienced operations and data management professionals, Seix has frequently ranked first quartile in both weighted average rating factor (WARF) and weighted average spread (WAS).1 WARF is a measurement that is used by credit rating companies to indicate the credit quality of a portfolio. This measurement aggregates the credit ratings of the portfolio's holdings into a single rating. WAS is the par-weighted average spread (generally above LIBOR) of the performing floating rate assets in the portfolio.

The Seix CLO approach to credit research allows for a conviction in credit selection during times of stress. As the team explained to prospective investors, its leveraged loan strategy aims to capture upside potential while limiting downside risk through rigorous fundamental credit analysis and a strict sell discipline. That translates into an ability to rotate capital effectively, monitor market excesses to identify market dislocations, find value in mispriced assets within out of favor sectors, and spot less trafficked potential opportunities in misunderstood industries.

Relative Performance Comparison

1Seix 2.0 CLOs included in the study: Mountain View CLO 2013-1 Ltd., Mountain View CLO IX Ltd., Mountain View CLO X Ltd., Mountain View CLO 2016-1 Ltd., Mountain View CLO 2017-1 Ltd. and Mountain View CLO 2017-2 Ltd., Mountain View CLO XIV Ltd.

2 Source: The CLO Manager Style Guide, Wells Fargo, October 28, 2019. Data is extrapolated from Intex, using median equity payments and portfolio statistics for all of the managers’ deals issued since 2011. Only equity payments which occur during the CLO’s investment period are included.

Past performance is not indicative of future results.

Late Innings Support

Research by S&P Global Ratings provided investors with additional perspective on the latest Mountain View offering, including cash flow projections, collateral quality, target collateral, credit enhancement, and obligor holdings (by sector). On January 3, 2020 (three weeks prior to when the deal closed), S&P issued an analysis2 of CLO transactions managed by Seix and its affiliate, Seix CLO Management LLC, since the financial crisis (“CLO 2.0”)3.

The S&P findings underscored Seix’s meticulous approach to CLO issuance and risk management.

Closing the Book

In the end, the Seix-Goldman team managed to find a new lead investor for the AAA tranche, and the total book of distribution consisted of 22 investors spread across the entire capital structure.

The final capital structure was as follows:

Source: Seix Investment Advisors

“The Seix-Goldman team put in a tremendous effort and were particularly innovative trying to satisfy unique investor needs,” said Wu.

Looking Ahead

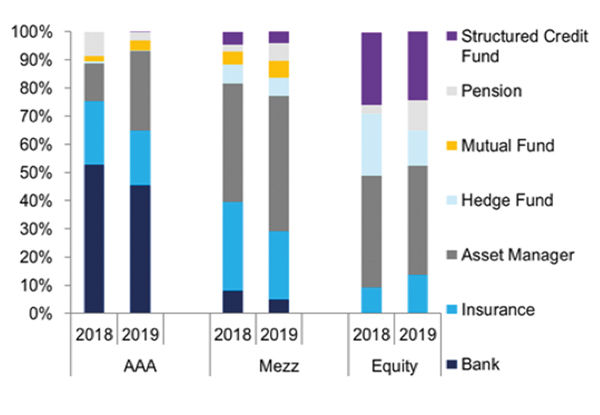

With CLOs becoming increasingly popular with a broad base of institutional investors (see Exhibit 1), Seix’s latest CLO succeeded in a crowded field. By the end of 2019, there were roughly 115 CLO managers, including 15 new players that entered the market that year. More entrants are expected to enter the market in 2020, ranging from large global asset management companies to small institutions backed by major insurance companies. Collaborations between large balance sheet financial institutions and CLO managers are likely to grow. Some CLO managers have also partnered with private equity shops, insurance companies, pension plans, and endowments.

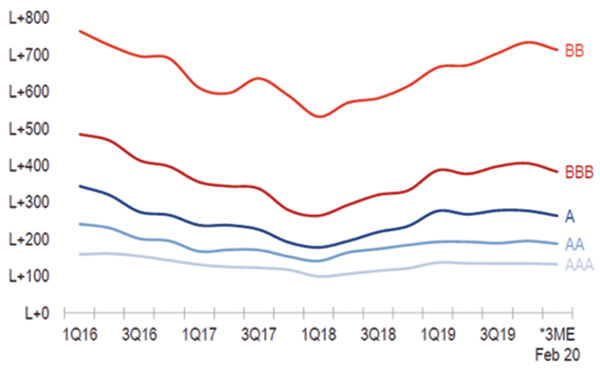

The floating rate CLO debt should remain popular with institutional investors, as it offers relative value compared with credit instruments of comparable ratings. (See Exhibit 2, which shows the average CLO coupon across the capital spectrum, according to S&P). As a result, we foresee greater institutionalization of CLO managers but continued opportunity for boutique shops with highly experienced teams with the potential to scale higher with institutional partners.

EXHIBIT 1. INVESTOR-TYPE BREAKDOWN OF

NEW-ISSUE U.S. CLOS

As of December 31, 2019

Source: Citi Research

EXHIBIT 2. AVERAGE US CLO COUPON

ACROSS THE STACK

*Excludes middle-market CLOs

Source: LCD, and offering of S&P Global Market Intelligence

*Data is through Feb 3, 2020