Don’t let record low rates sway you. High yield still has the potential to enhance income and total return, lower interest rate volatility, and diversify risk in fixed income portfolios.

With rates anchored lower for the foreseeable future, fixed income investors seeking more yield only have a few levers to pull—extend duration, take more credit risk, or venture into currency/country risk (via emerging markets) as the volume of negative yielding debt around the world has hit a record $18 trillion.

Enter high yield, a category that has demonstrated compelling risk-adjusted returns over multiple market cycles with significantly lower duration (3.56 years) than investment grade bonds (8.83 years), according to Bloomberg.

High Yield Bonds Deliver Competitive Returns Per Unit of Risk

Source: Standard & Poor’s, FTSE Russell, Bloomberg Barclays

Past performance is not indicative of future results.

The High Yield, Leveraged Loan, Large Cap Equity & Small Cap Equity Markets are represented by the Bloomberg Barclays U.S. Corporate High Yield Index, S&P 500® Index & the Russell 2000® Index, respectively. Returns were calculated using monthly and begin with the inception of the Credit Suisse Leveraged Loan Index on 1/1/92.

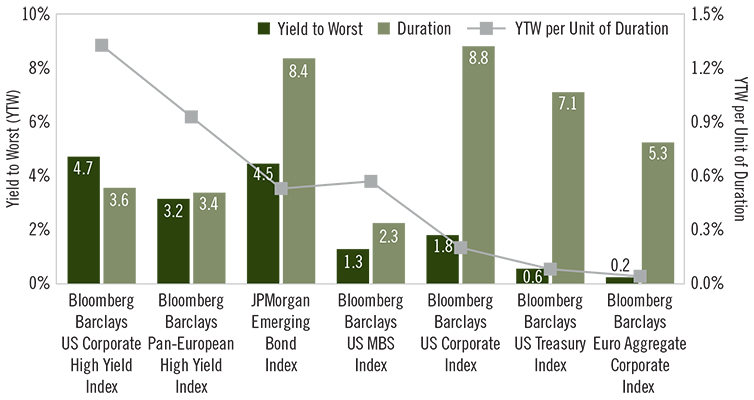

Granted, massive inflows into high yield have driven yields down lately, but the asset class remains durable. As the chart below shows, the yield to worst from U.S. high yield corporate bonds (as represented by the Bloomberg Barclays U.S. Corporate High Yield Total Return Index) was 4.72% as of 11/30/20—more than double that of investment grade corporates’ YTW of 1.8% (as represented by the Bloomberg Barclays U.S. Corporate Investment Grade Bond Index), to cite just one example. (See chart below.)

U.S. Corporate High Yield Still Exhibits Favorable Yield and Duration Characteristics

Yield to worst (YTW), duration in years, YTW per unit of duration

Source: Bloomberg and JPMorgan. Data as of 11/30/20. Underlying Indexes represented in chart are defined below.

Scoping Opportunity

Our recent focus has been identifying the hardest hit sectors due to the shutdown of the economy to identify good businesses with ample liquidity to make it through the economic slowdown. Our expectation is that many of these credits will bounce back strongly once we get to the “new normal”. Since November 9 (when Pfizer announced significant progress with its COVID vaccine candidate), we have been reducing our exposure to these resilient sectors/credits and are now about 1.5x the benchmark weight. We have also been buying more defensive names as we sell our COVID credits. From the perspective of 12 to 18 months, the COVID bucket remains the area that we believe offers the best potential value, but we will likely continue to reduce into strength so we have room to add if we experience some market volatility.

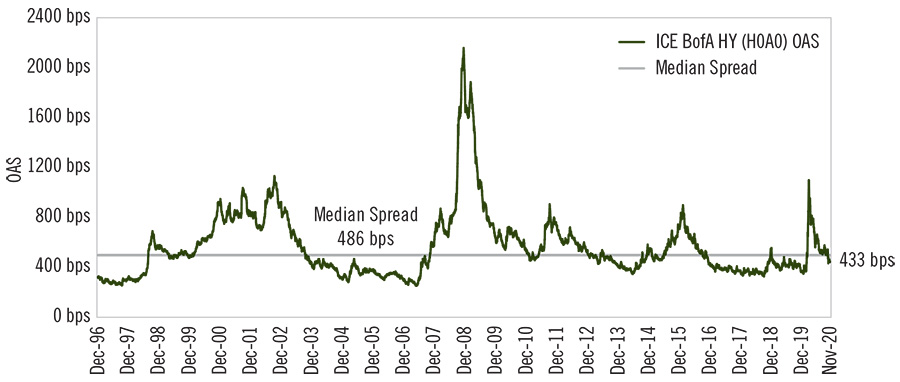

From a valuation perspective, we are still about 75 bps wide on an option adjusted spread basis relative to where we began the year (we were tighter than that in 1Q). This is despite the high overall default rate cleansing the weakest credits from the asset class in addition to the significant fallen angels that brought former investment grade credits into high yield. On an apples-to-apples basis, we have some room to run to get back to where we were in January.

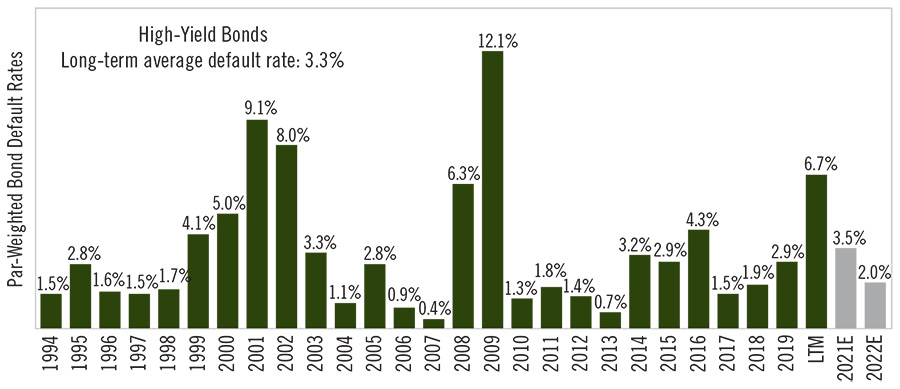

Defaults Appear to be Heading Lower

Includes distressed exchanges. Source: JPMorgan. Data as of 11-30-20.

Outlook

We believe the economic growth through 2021 and into 2022 should be solid and defaults should peak soon if they have not already. (Note: November was the first month without any default activity since August 2018.) This should provide a decent backdrop for some continued spread tightening. Further, increased profitability/productivity could be a positive surprise as we get to the “new normal”. As an example, regional gaming companies are suggesting they can operate profitably at 50% of historical revenue, and we are hearing similar assertions from other companies.

Having said that, we could see some volatility due to: rising COVID cases and deaths resulting in regional shutdowns and/or increases in restrictions; Georgia elections; potentially disappointing vaccine news in terms of rollout, and/or efficacy; or disappointments with additional stimulus. However, we would generally consider market volatility as an opportunity to add some yield.

High Yield Spreads Offer an Attractive Entry Point

Past performance is not indicative of future results.

Source: ICE BofA Indices as of 11/30/20

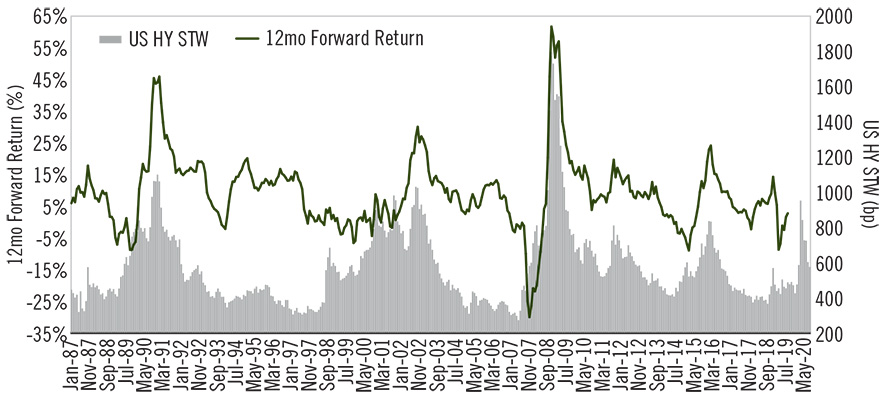

Current High Yield Spreads Still Offer the Potential for Robust Long-Term Total Returns

U.S. High Yield Spread to Worst Vs. 12-Month Forward Return

Past performance is not indicative of future results.

The J.P. Morgan U.S. High Yield Index is designed to mirror the investable universe of the U.S. dollar domestic high yield corporate debt market. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Source: JPMorgan analysis as of 8/31/20

The Takeaway

High yield can still offer a compelling way for fixed income investors to pursue higher long-term returns than is available in most other fixed income sectors (for those willing to accept higher volatility) AND a way for equity investors to trim their allocations and pursue decent longer term returns with an expectation of lower volatility.

Of course, the risk/reward relationship and the prospect for elevated volatility in high yield can’t be ignored. This environment demands differentiated active management, meticulous bond-by-bond research, and a selective approach focused on quality.

The commentary is the opinion of the subadviser. This material has been prepared using sources of information generally believed to be reliable; however, its accuracy is not guaranteed. Opinions represented are subject to change and should not be considered investment advice or an offer of securities. Forward-looking statements are necessarily speculative in nature. It can be expected that some or all of the assumptions or beliefs underlying the forward-looking statements will not materialize or will vary significantly from actual results or outcomes.