Obsession with liquidity via money market funds comes at a price, which is why investors may want to consider short- and ultra short-term bond funds with higher yields as rates stay lower for longer.

When markets sold off last March, many investors fled to highly liquid money market funds (MMFs) as a cash management tool, only to see yields plummet to pitiful lows, underscoring the epithet, “cash is trash.”

According to the Investment Company Institute, the amount of cash parked in retail and institutional1 MMFs2 totaled $4.33 trillion as of November 11. The average interest rate for non-jumbo money market funds (under $100,000) was seven basis points better than the proverbial mattress.

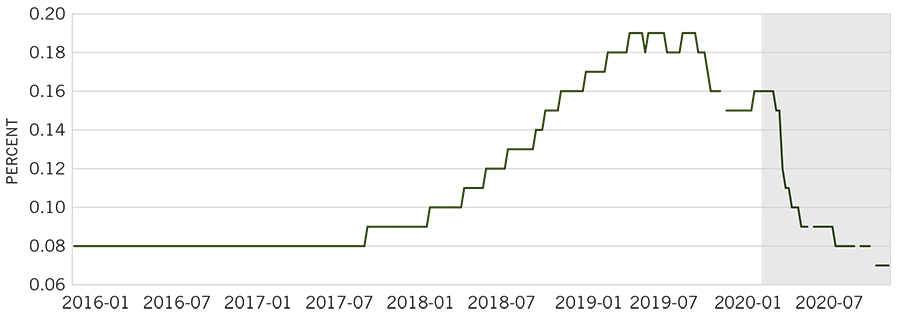

National Rate on Non-Jumbo Deposits (less than $100,000): Money Market

Source: Federal Deposit Insurance Corporation

Past performance is not indicative of future results.

Note: The national rate is calculated by the FDIC as a simple average of rates paid (uses annual percentage yield) by all insured depository institutions and branches for which data are available. Data used to calculate the national rates are gathered by RateWatch.

Savings and interest checking account rates are based on the $2,500 product tier while money market and certificate of deposit are based on the $10,000 and $100,000 product tiers for non-jumbo and jumbo accounts, respectively. Account types and maturities are those most commonly offered by the banks and branches for which data is available – no fewer than 49,000 locations and as many as 81,000 locations reported. The deposit rates of credit unions are not included in the calculation.

Talk about an opportunity cost. Not only did investors who fled stock funds miss out on the dramatic rebound that ensued into early fall; they also missed the potential for higher levels of current income and total return from short or ultra short duration bond strategies with less market risk and lower volatility than bond funds with longer maturities. Granted, past performance is no indication of future results, but the key point here is that investors who chose short-and ultra-short-term funds over money market funds realized the potential for higher yields.

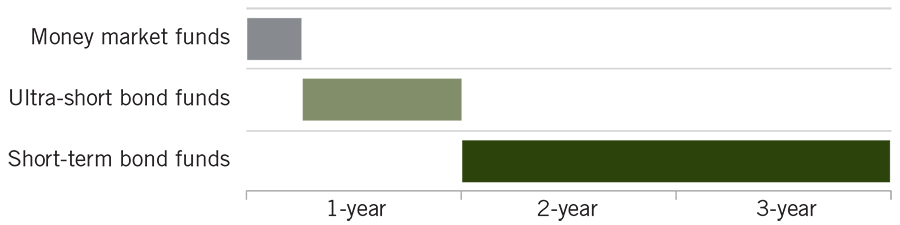

Money Market Funds’ Duration Generally Pale Compared to Short- and Ultra-Short-Term Funds

Short-term bond fund duration

Source: Securities and Exchange Commission. For illustrative purposes only.

Short duration strategies typically include a well-diversified portfolio of short- to medium-term corporate bonds, asset-backed securities, mortgage-backed securities, U.S. Treasuries, and U.S. government agency debentures with the potential to yield considerably more than shorter-term Treasury bills. But a word of caution: in reaching for yield, some strategies may increase their risk exposure with lower-rated credits and less liquid structured products. Therefore, investors need to ask how such strategies have protected in down markets. The answer, in some cases, may come as a negative surprise.

In contrast, some ultra short managers have benefitted this year from agency commercial mortgage-backed securities (CMBS, to cite one example) thanks to the Federal Reserve’s coronavirus stimulus measures, which helped fuel a rally in mortgage bonds guaranteed by government agencies Ginnie Mae, Fannie Mae and Freddie Mac.

Of course, the relative attraction of one asset class over another may vary over time, in which case a manager may seek to reduce risk over the short term in order to maximize income over the long term. In times of extreme valuations or market chaos, it may be wise to rotate more into Treasuries.

The potential to earn more income in short- or ultra-short duration fixed income strategies than money market funds hinges on diversification, high portfolio quality, low risk structures, liquidity and transparency. Indeed, in a lower for longer interest rate environment, a disciplined sale is as important as a winning purchase.

However, the key is getting investors comfortable moving out of the money market space, especially with the Fed likely to hold rates near zero for a long time. Even if an ultra-short strategy only gets them +50 bps over the 10 bps (or less) sweep vehicle yield, when multiplied by, say, five or six years of the Fed’s zero interest rate policy, investors mindful of the additional risk may have at least picked up a few percent on their liquidity sleeve assets. All of which may help to explain why some institutions are segmenting their cash allocations according to anticipated needs over several time horizons.

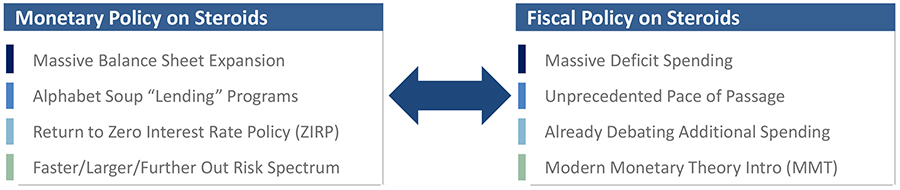

Lower for Longer 3.0 – Post Covid vs. Post GFC

Unprecedented Monetary & Fiscal Policy Responses to COVID-19 Further Solidifies an Extended/Coordinated Lower for Longer Thesis

1 ICI classifies funds and share classes as institutional or retail based on language in the fund prospectus. Retail funds are sold primarily to the general public and include funds sold predominantly to employer-sponsored retirement plans and variable annuities. Institutional funds are sold primarily to institutional investors or institutional accounts purchased by or through an institution such as an employer, trustee, or fiduciary on behalf of its clients, employees, or owners.

2 Data for exchange-traded funds (ETFs) and funds that invest primarily in other mutual funds were excluded from the series.