Key points on the forthcoming shift to a new interest rate benchmark

Should leveraged loan investors be concerned about the end of LIBOR?

Seix believes the loan market will be prepared for the cessation of LIBOR and transition to SOFR. Companies have already begun announcing plans to issue loans tied to SOFR with Ford’s refinancing of its revolving credit facility and Walker & Dunlop’s new-issue term loan B priced this year.

Here’s some useful background:

What is LIBOR and why does it matter for leveraged loan investors?

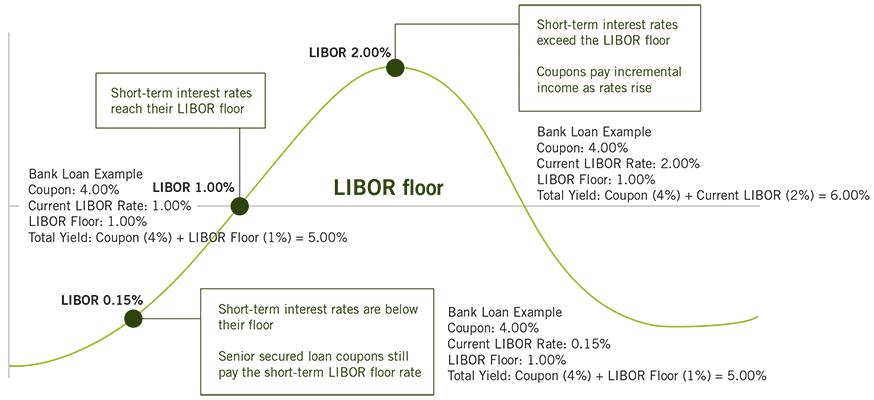

LIBOR, or the London Interbank Offer Rate, is one the most widely recognized interest rate benchmarks used to value a wide range of financial products, such as leveraged loans. As a floating rate asset class, loans reset monthly or quarterly to a spread over a base rate – LIBOR. As rates rise, loans benefit by receiving additional incremental yield tied to LIBOR. For example, if short term rates (LIBOR) rise 1.00%, loan investors will receive an additional 1.00% of yield when the loan resets. Loans are also often issued with a LIBOR floor, which includes a minimum spread level above LIBOR when interest rates are low.

Why and when is LIBOR ending?

A widespread LIBOR-rigging scandal was exposed in 2012 that led to convictions for some traders and penalties to several banks. Regulators moved to end LIBOR after concluding it was unreliable and prone to manipulation.

The ICE Benchmark Administration (IBA), the administrator of LIBOR, and the UK’s Financial Conduct Authority (FCA) announced that the publication of USD LIBOR will cease after June 30, 2023. Additionally, Federal regulators have stated that there are safety and soundness risks with the continued use of LIBOR and advised banks to stop entering new contracts with LIBOR reference rates by December 31, 2021.

What is replacing LIBOR?

The Secured Overnight Financing Rate (SOFR) is widely accepted as the LIBOR replacement for loans. SOFR is based on overnight Treasury Repo Rates with nearly $1 trillion of underlying daily transactions and not subject to market manipulation. Since SOFR is a daily rate, Term SOFR was developed as a forward-looking rate from SOFR futures trading. Additionally, since LIBOR assumes a level of embedded credit risk, while SOFR is a secured, or risk-free rate, a constant spread adjustment will apply based on the average 5-year lookback of LIBOR, meant to capture the long-term difference between LIBOR and SOFR. For example, as of September 30, 2021, the current reference rate would be 31 bps [SOFR (5 bps) + spread adjustment (26 bps)].

London Interbank Offered Rate (LIBOR): A benchmark rate that some of the world’s leading banks charge each other for short-term loans and that serves as the first step to calculating interest rates on various loans throughout the world.

Credit & Interest: Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a debt security may fail to make interest and/or principal payments. Values of debt securities may rise or fall in response to changes in interest rates, and this risk may be enhanced with longer-term maturities. Bank Loans: Loans may be unsecured or not fully collateralized, may be subject to restrictions on resale, and/or trade infrequently on the secondary market. Loans can carry significant credit and call risk, can be difficult to value, and have longer settlement times than other investments, which can make loans relatively illiquid at times. Foreign & Emerging Markets: Investing internationally, especially in emerging markets, involves additional risks such as currency, political, accounting, economic, and market risk. High Yield-High Risk Fixed Income Securities: There is a greater level of credit risk and price volatility involved with high yield securities than investment grade securities. Liquidity: Certain securities may be difficult to sell at a time and price beneficial to the fund. Leverage: When a fund leverages its portfolio, the value of its shares may be more volatile and all other risks may be compounded. Market Volatility: Local, regional, or global events such as war, acts of terrorism, the spread of infectious illness or other public health issue, recessions, or other events could have a significant impact on the fund and its investments, including hampering the ability of the fund’s portfolio manager(s) to invest the fund’s assets as intended. Exchange-Traded Funds (ETF): The value of an ETF may be more volatile than the underlying portfolio of securities it is designed to track. The costs of owning the ETF may exceed the cost of investing directly in the underlying securities. Market Price/NAV: At the time of purchase and/or sale, an investor’s shares may have a market price that is above or below the fund’s NAV, which may increase the investor’s risk of loss.

Not all products or marketing materials are available at all firms.

Not insured by FDIC/NCUSIF or any federal government agency. No bank guarantee. Not a deposit. May lose value.