Fallen angels are multiplying exponentially. The best time to buy such bonds at attractive levels, in our view, is just before they get downgraded, since some high yield managers can’t buy investment grade.

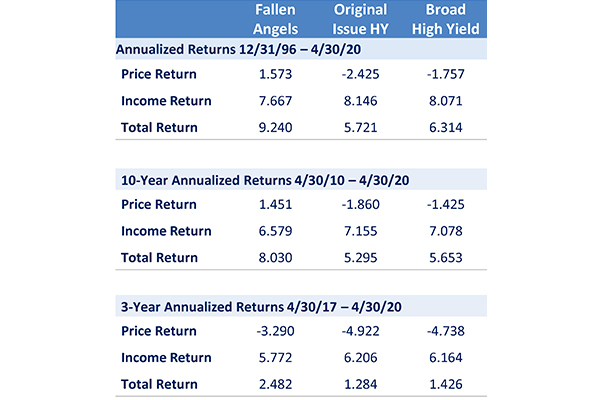

We believe investors can potentially generate equity-like returns in certain fallen angel or potential fallen angel bonds, with less risk than equities. While current valuations remain attractive, Exhibit 1 shows that fallen angels have shown significant outperformance over long (and shorter) periods of time.

As cited below, income return is a proxy for a high yield bond’s coupon. Fallen angels have a lower income return versus originally issued yield. But the price return is actually positive versus originally issued high yield that is coupon-minus. While most high yield managers over the years have focused on yield by regularly clipping coupons and truncating that downside, they were less concerned with total return. But yield is only part of the picture. Total return potential tells the entire story.

Exhibit 1. Focus on Total Return

Past performance is not indicative of future results. Source: Seix analytics; Fallen Angels – ICE US Fallen Angel High Yield 10% Constrained Index (H0CF); Original issue HY – ICE BofA Original Issue High Yield Index (H0HY): Broad High Yield – ICE BofA US High Yield Index (H0A0). As of 4/30/20.

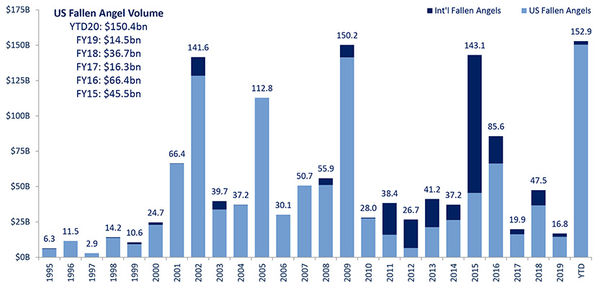

A Much Bigger Pond to Fish In

Through the first five months of 2020, the volume of fallen angels, bonds that descended from investment grade to high yield, was more than 10 times higher than all of 2019. (See Exhibit 2.)

Exhibit 2. Fallen Angel Volume Forecast:

to Exceed 2009 Levels

Source: JPMorgan as of 4/14/20

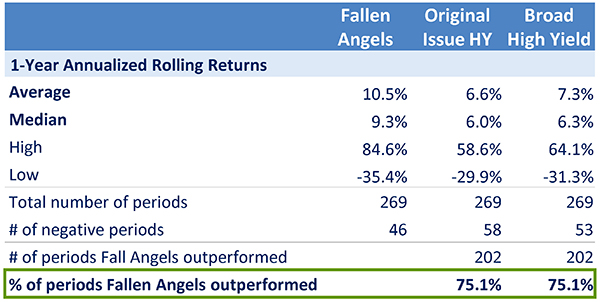

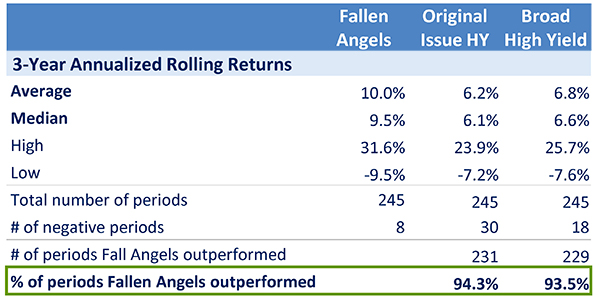

Historical Performance is Encouraging

The sheer growth of fallen angels spells considerable potential opportunities for nimble managers with rigorous research that can spot relative values and manage risk. While past performance is no guarantee of future results, consider the historical results of fallen angels shown in Exhibits 3 and 4. According to Seix analytics, fallen angels one-year annualized rolling returns outperformed 75% of the time. Three-year annualized rolling returns outperformed 94% of the time.

Exhibit 3. Fallen Angels Outperformed 75% of the Time1

Exhibit 4. Fallen Angels Outperformed 94% of the Time2

1 Since inception of the Fallen Angel Index (H0CF) 12/31/96, using monthly rolling 1-year periods.

2 Using monthly rolling 3-year periods.

Past performance is not indicative of future results.

Seix: Seix analytics; Fallen Angels – ICE US Fallen Angel High Yield 10% Constrained Index (H0CF); Original issue HY – ICE BofA Original Issue High Yield Index (H0HY): Broad High Yield – ICE BofA US High Yield Index (H0A0). As of 4/30/20.

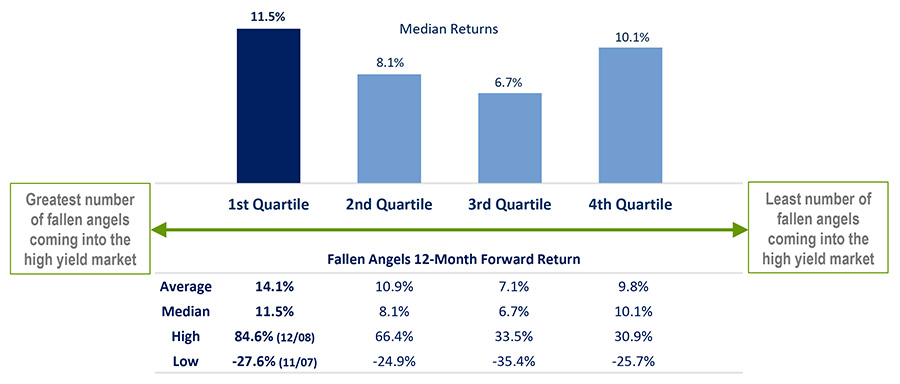

Timing Matters

Since the investment grade market tends to “shoot first and ask question later,” increasing volumes of investment grade downgrades tend to benefit high yield managers as illustrated in Exhibit 5. This shows that the best time to invest in fallen angels is when a lot of fallen angels are coming into the market. The first quartile depicts when the greatest amount of fallen angels were coming in. The fourth quartile shows when there were no fallen angels coming into high yield.

Exhibit 5. The Best Time to Invest in Fallen Angels

Is When Downgrades Is High

Note: Quartiles categorized based on monthly total par dollarvolume of bonds downgraded to fallen angels, with 1st quartile having the highest dollar amount and the 4th quartile with the lowest dollar amount.

Past performance is not indicative of future results.

Source: Seix analytics; Fallen Angels – ICE US Fallen Angel High Yield 10% Constrained Index (H0CF) as of 4/30/20.