After a depression-like collapse and an epic response from monetary and fiscal authorities, the hobbled economy raises serious questions about liquidity issues morphing into solvency crises in some sectors.

By James Keegan, Chief Investment Officer, Chairman

In Brief:

> With sharp drops in retail sales, industrial production and capacity utilization, second-quarter gross domestic product (GDP) could drop as much as 45%.

> While all the liquidity created by the Federal Reserve (Fed) has certainly helped calm the markets, one must wonder what happens if the liquidity crisis of March morphs into a solvency crisis later in the year and beyond as companies’ revenues, earnings and cash flows remain under pressure during the worst recession/ possible depression since the 1930s.

> Recent stock market gains have been led by a handful of stocks—indeed, an even smaller concentration than the so-called “Nifty Fifty” of the '60s and '70s. Below the surface many economically sensitive sectors remained well into bear market territory.

> Rigorous underwriting and portfolio construction are the hallmarks of our process and have dictated the securities we have added post-crisis repricing. Fed buying has helped matters, but solvency risk remains elevated given the extent of economic damage and overleveraged balance sheets.

While the Bloomberg consensus has GDP contracting just under 6% this year—the worst contraction in the post-war period—it is entirely possible that the U.S. economy could contract on the order of 8-10%. With more than 36 million people unemployed (as of May 18), Federal Reserve Chair Jay Powell recently told “60 Minutes” the jobless rate likely will peak around 25%, which of course would exacerbate pressure on consumption, delinquencies, and defaults within the household sector.

We’ve already seen sharp declines in retail sales, industrial production, and capacity utilization rates. Car sales in April were approximately half the seasonally adjusted annual rate of February. As a result, second-quarter GDP could plunge 30-40%, according to consensus estimates. (Our estimate is as much as 45%.)

All of which points to a greater risk of deflation as recession takes hold, although the gradual re-opening of various regions and sectors has fueled expectations of an economic rebound in the third quarter. The big question, though, is what happens in the fourth quarter and beyond, especially if there is a second wave of COVID-19 infections and a viable vaccine or treatment remains on the horizon as health experts expect. A second lockdown would be an economic disaster, which we expect would further decimate small businesses that survived the first lockdown. Small businesses are the job creation engine of the U.S. economy and, as such, have significant economic consequences for the economy, given consumption is 70% of the economy.

In any case, significant and potentially secular changes in consumer and corporate behavior seem likely. How they play out (and to what degree) is another matter. The “unknown unknowns" (a term popularized by former Secretary of Defense Donald Rumsfeld) are pretty big right now.

The Fed’s Heavy Backstop

In the face of unprecedented liquidity challenges, the Fed's balance sheet has expanded to $6.9 trillion in nine weeks—a 61% increase. It has started buying investment grade and high yield ETFs, and the expectation is that we will likely end 2020 with a Fed balance sheet of about $9.5-10.5 trillion (up 140% for the year).

While all that liquidity created by the Fed has certainly helped calm the markets, one must wonder what happens if the liquidity crisis of March morphs into a solvency crisis later in the year and beyond as companies’ revenues, earnings and cash flows remain under pressure during the worst recession/ possible depression since the 1930s. Fiscal authorities would have to step in again. That means going beyond the CARES Act which calls for $2.9 trillion of stimulus—13.5% of U.S. GDP.

Granted, the additional $3 trillion stimulus recently approved by the House will be dead on arrival in the Senate, but we could see something more along the lines of an infrastructure bill, although this would be more likely after the election in 2021. There could also be more aid to small businesses and unemployment insurance, since the CARES Act carries unemployment coverage through the end of July.

Political wrangling over unemployment will no doubt escalate. After all, a study from the University of Chicago estimates that nearly two-thirds of the people collecting unemployment benefits now are making more than they did when they were employed and some of those people may not want to return to work, particularly if contagion remains a significant risk factor. At any rate, that same study estimates that 42% of recent pandemic-induced layoffs will result in permanent job loss.

Against that backdrop, we find a significant divergence between the stock market and actual corporate profits and cash flow. Clearly, the NASDAQ and the Standard & Poor’s 500® are being led by a handful of stocks—indeed, an even smaller concentration than the so-called “Nifty Fifty” of the '60s and '70s. Below the surface, many economically sensitive sectors (e.g., banks, financials, cap goods, and transportation) remained well into bear market territory. In contrast, the S&P 500 was down 11% on a cap-weighted basis, but on an equal weighted basis, it was minus 21%.

What Shape Will Recovery Take?

There appears to be strong consensus that the current slump will become the deepest economic contraction since the Great Depression, both from an industry perspective and a geographic perspective. How long will it last? According to a recent survey of institutional investors, 52% of the respondents expect a U-shaped recovery, and 22% expect a W-shape recovery. In the minority, only 15% were expecting a V-shaped recovery (we assume that number would be lower today), and 7% were anticipating an L-shaped recovery.

Our view is the risk of a reverse J-type (or fish hook) recovery, as this is not a garden variety recession that would be over in two to three quarters. Given the potential secular changes brought on by the pandemic’s impact on consumer behavior (more saving, less spending) and corporate behavior (resiliency over efficiency and stakeholders over shareholders), the risk is a deep recession turning into a depression. But unlike the Great Depression of the 1930s, this dire scenario, if it unfolds, would be tempered by the unprecedented fiscal/ monetary response as well as the safety net in place like FDIC insurance.

Surveys show that many people will be reluctant to go to restaurants, malls, concerts, and sporting events. Additionally, people's reluctance to get on a flight and travel somewhere could have long lasting implications as we saw post-9/11, particularly impacting business travel, convention travel, and those industries that serve such customers. Meantime, working from home, videoconferencing, and tele-commuting has implications for commercial real estate.

On the corporate side, look for supply chains to be altered and more diversified, with resiliency taking greater precedence than efficiency. Case in point: Taiwan Semiconductor’s recent decision to build a $12 billion chip fabrication facility in Arizona.

Also, look for managements to increase their focus on stakeholders such as employees, customers, and suppliers rather than just exclusively being focused on shareholders. At the same time, balance sheet strength, credit ratings, and liquidity are going to become extremely important. That should translate into dividend cuts and fewer share buybacks, unlike this past cycle when the largest buyers of equities were corporations buying back their own shares to the tune of over $5 trillion.

Corporate Binge Borrowing

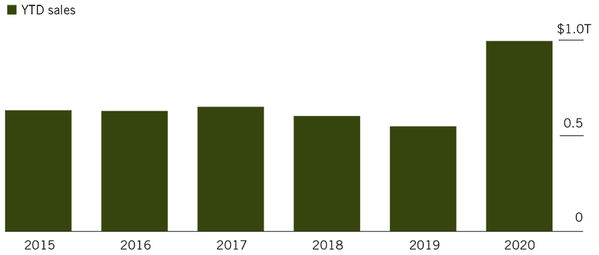

Corporate debt as a percentage of GDP is at a record high, and while sales of investment grade (IG) bonds have reached a torrid pace (see Exhibit 1), the quality of the IG market is as low as it's ever been. About 60% of the non-financial corporates are BBB rated. Before the coronavirus hit the markets, about a third of those BBB non-financials had leverage statistics that the rating agencies openly told us were inconsistent with an investment grade rating and more consistent with a non-investment grade rating. A number of issues were already on watch for a downgrade or had a negative outlook, which helps to explain why the Fed went as far it did to buy corporate bonds, down to fallen angels (as low as Ba3/ BB-) and high yield via ETFs.

Record Rate (Exhibit 1)

U.S. investment-trade sales hit $1 trillion at fastest pace

Source: Bloomberg

Weaker Fundamentals vs. Stronger Technicals

Although corporate bond fundamentals are deteriorating, the technicals are very positive right now because of the Fed’s overt support via its PMCCF (Primary Market Corporate Credit Facility) and SMCCF (Secondary Market Corporate Credit Facility) programs. After a dramatic sell off in investment grade and high yield in Q1, spreads are tighter, but both remain above long-term averages.

Still, leverage in the investment grade corporate market, which was already at a record high pre-COVID shutdown, is now even higher with record corporate bond issuance in March, April and May. However, in an environment where the Fed has said that it will buy corporate bonds, it is this factor that takes precedence in the short term over deteriorating fundamentals in terms of lower earnings, higher leverage, deteriorating cash flow, and reduced interest coverage.

Risk Aversion

With leverage-adjusted spreads close to record tights pre-COVID lockdown, we were positioned with a large underweight of risk going in to the March selloff/ repricing. And the biggest underweight in our Aggregate Bond-type portfolios was about a 50% benchmark weighting in the corporate bond sector. Our investment strategy of being significantly underweight the corporate sector and overweight the U.S. Treasury sector paid off in two ways: 1) our portfolios benefitted from the flight to quality demand for U.S. Treasuries that resulted in higher U.S. Treasury bond prices; and 2) we were able to cover our underweight in corporate bonds at much wider risk premiums.

Rigorous underwriting and portfolio construction are the hallmarks of our process and have dictated the securities we have added post-crisis repricing. Fed buying has helped matters, but solvency risk remains elevated given the extent of economic damage and overleveraged balance sheets.

Default Outlook

Now that the Fed has drawn the line on corporate bonds it is willing to purchase in the primary or secondary market, it's fair to say that defaults will likely accelerate. As the Bank for International Settlements puts it, 15% of global corporations can be defined “zombie”-like, which is to say they have an interest coverage ratio of less than one.

As a result, we are not contemplating any dramatic broad-based overweight at these levels, largely a function of earnings and cash flow remaining under pressure on the heels of mounting leverage in the investment grade corporate market.

Seeking Returns per Unit of Risk

As adherents to the full market cycle investment discipline, we differ from many of our competitors who tend to buy risk/yield until the music stops and, as such, are not in a position to take advantage of repricings/dislocations such as full-cycle investors like Seix. We understand that when we're underweight risk, we're giving up some short-term income (or opportunity cost). The key is taking risk when returns per unit of risk are attractive and reining in risk when returns per unit of risk are unattractive, and preserving clients’ capital is of paramount importance.

Negative Rates

While we take the Fed’s desire to avoid negative policy rates at face value, it is possible that Treasuries up to 10 years could trade with negative yields like they do in Europe and Japan, particularly if we get the deflationary wave we expect in this severe economic contraction. (European bond markets have been in a negative rate environment for five-plus years, Japan has been in and out of negative rates for the last 20 years.)

In that scenario, investors would not be relying on income anymore; they would be relying on capital appreciation from declining bond yields. It all has to do with bond math and convexity: As of May 15, long Treasuries were up 22.9% this year, and that's with rates at very low levels. Sure, convexity can hurt should long-term bond yields rise, but at this point we do not anticipate long-term bond yields rising much at all. However, we can envision long Treasuries trading below 1%.

Income then would have to come from the spread sectors; i.e., corporate bonds, residential mortgage backed securities, commercial mortgage backed securities, asset backed securities, even (potentially) municipal bonds. Continuing our emphasis on quality, we’ve been concentrating on AAs down to high quality BBs that meet our rigorous underwriting criteria.